Learn How to Calculate your Annual Panama Real Estate Taxes (effective Jan 2019):

In Panama, real estate tax, also known as property tax, is not municipal, but national and the entity responsible for its collection is the Ministry of Economics and Finance located on Ave. Peru, in Panama City. It must be paid according to the official assessment value, which is usually the declared value on the sale document.

Real estate located in Panama, whether urban or rural, is subject to property taxes.

The tax base depends on the total value of the land, plus all improvements, as appraised by Land Commission (Oficina de Catastro), and if it is your principal residence, second residence, commercial, etc.

Real estate transactions at prices above the appraisal value automatically increase their value for tax purposes.

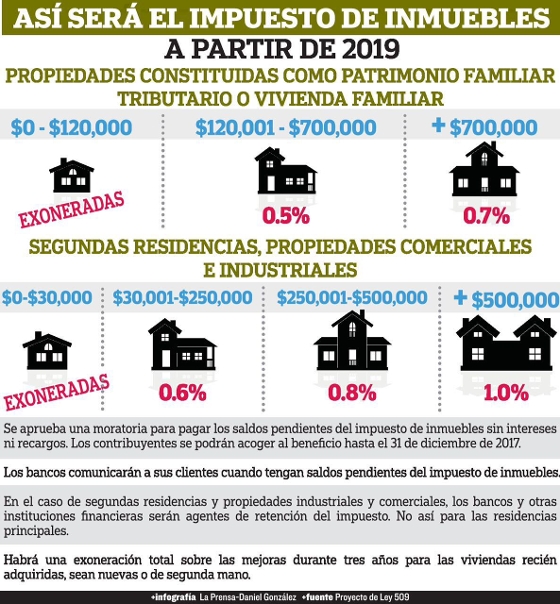

The maximum annual percentage of assessment on a primary residence is .7%, which is based upon two items:

- Over the value of the land, and

- Over the declared value of the improvements built.

The taxable base will depend upon the total value of the land plus all improvements. The following is a complete breakdown of property tax rates under the new property tax law:

For your primary residence:

Properties currently under the old 20 year property tax exemption will continue to enjoy those benefits. If your property is not applicable for the 20-year tax exemption, then the following revised Panama property tax exemption exists:

Property Tax Exemption: Residential

- 15 years Up to US$ 100,000.00

- 10 years From US$ 100,000.00 to US$ 250,000.00

- 5 years Above US$ 250,000.00

- Commercial Use/Non-residential improvements have 10 year exoneration no matter property value

Taxes can be paid in three installments, namely by April 30th, August 31st, and December 31st.

Right of Possession (ROP) properties do not incur property taxes, since the property technically belongs to the government of Panama. Property taxes cover the fiscal year that runs from July 1 to June 30.

Individuals also can pay half of their property taxes on or before August 15, and pay the other half on or before January 15 without interest and penalty.